For years, packaging decisions in the United States were made based on commodity costs and on-shelf visibility, ignoring end-of-life costs entirely. Most producers don’t know the true cost of their packaging. EPR fees will tell them before their competitors notice.

Having worked inside one of the world’s largest consumer goods companies and as a founding team member of the organization, now setting EPR fees in multiple states, I’ve watched these two worlds operate in parallel with limited ways to collaborate. The gap between product performance on the shelf and recyclability is closing faster than most corporate packaging teams realize. Companies currently building their 2028 packaging roadmaps are making decisions that will determine their EPR cost structure when full multi-state programs are live. 2032 is California’s deadline requiring all packaging sold into the state to be considered recyclable, and it is only 4 to 6 planning cycles away, depending on your company’s innovation cycle.

To put it plainly: the recyclability label on a package is not sufficient. What EPR programs evaluate, and what the fees reward, is whether a material can be collected, sorted, processed, and delivered to a verified end market at scale. Many materials that carry recyclability claims do not meet that threshold under EPR program definitions. The fee structure reflects that gap directly.

What EPR Fees Actually Incentivize: Recyclability

EPR fees are not arbitrary. In Colorado and Oregon, where programs are now invoicing producers, fee rates are set through a structured process that accounts for actual system costs: collection, sorting, processing, and delivery to responsible end markets. Circular Action Alliance (CAA) is the approved Producer Responsibility Organization across active state programs and is obligated to set fees based on anticipated program costs. While data inputs are still maturing, the methodology is structured to skew fees toward materials that cost more to recover and sell to a verified end market.

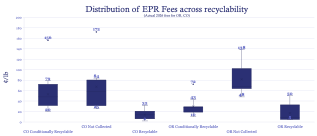

The result is a fee structure that reflects something the market has never formally priced: how hard your packaging is to recover. Current 2026 fee data tells a clear story. Materials classified as “not collected,” meaning no verified collection pathway exists under the program, carry fees reaching $1.72 per pound for polystyrene foam in Colorado. Recyclable materials carry significantly lower rates. The materials with the highest fees include flexible film, multi-material fiber and plastic packaging, mixed polymers, wood-based packaging, and certain plastic polymers, where no viable commodity market exists to offset system recovery costs. For a mid-size producer with significant volume in hard-to-recycle formats, the difference between recyclable and non-recyclable classifications can amount to hundreds of thousands of dollars annually per state.

That gap is the signal.

What the Signal Is Saying

The fee differential is not punitive in design. It reflects a real cost that existed long before EPR, one that municipalities and taxpayers were absorbing invisibly through landfill tipping fees. EPR makes these costs visible and routes them back to the producers whose packaging decisions created them.

If EPR fees are seen as a tax, the appropriate response is to minimize them through negotiation or accounting. If they are seen as a market signal, the appropriate response is to use them as input into packaging strategy, financial planning, and material innovation decisions.

The companies getting ahead of this are already doing the latter. They are mapping their packaging portfolios against state-specific recyclability classifications, modeling where fees are hitting hardest, and asking their design and supply chain teams questions that sustainability departments alone cannot answer: What is our cumulative fee differential if we stay in this format? What is the break-even point if we transition to a more recyclable alternative? Which materials are close to becoming recyclable? What industry actions can we support to mitigate our risks?

These are financial planning questions that EPR has made urgent.

The Multi-State Compounding Effect

For producers operating across the country, the signal gets louder as more states activate. California, Colorado, Oregon, Minnesota, Maine, Maryland, and Washington all have EPR programs at various stages of implementation. Each state has its own fee structure, its own recyclability classifications, and its own timelines, but the direction is consistent.

A packaging format carrying a high fee rate in Colorado will almost certainly carry elevated costs in other states where access to recycling is similarly limited. The compounding effect of multi-state fee exposure is where the financial stakes become significant enough to drive real packaging decisions.

A company that transitions out of a hard-to-recycle format now, before full programs are live across multiple states simultaneously, captures savings that a reactive competitor will pay for years. Where a recyclable alternative doesn’t exist, that’s precisely where pre-competitive industry action becomes critical.

Reading the Signal Correctly and Acting on It

EPR fees are the market finally pricing what recyclability actually costs the system. That pricing is imperfect and still evolving. Definitions vary by state, eco-modulation frameworks are being refined, and end-market standards are still developing.

For producers, the implication is straightforward. EPR fees tell you which parts of your portfolio are exposed. Industry coalitions are already working on pathways to reduce that exposure at the infrastructure level. The question is whether your company is contributing to that work and benefiting from it, or waiting to pay fees that result from not engaging.

The producers who treat this signal as strategic input and engage with industry efforts to build the infrastructure that makes recyclability real will build cost advantages that compound as the system matures. Those who wait for perfect information will react to invoices rather than plan around them.

EPR is not asking companies to be perfect. It is asking them to be honest about what their packaging actually costs the system, and to start making decisions accordingly.

{kind=link}